Union Finance Minister Nirmala Sitharaman with Minister of State for Finance Pankaj Chaudhary addresses a press conference in Mumbai on February 4, 2023.

| Photo Credit: PTI

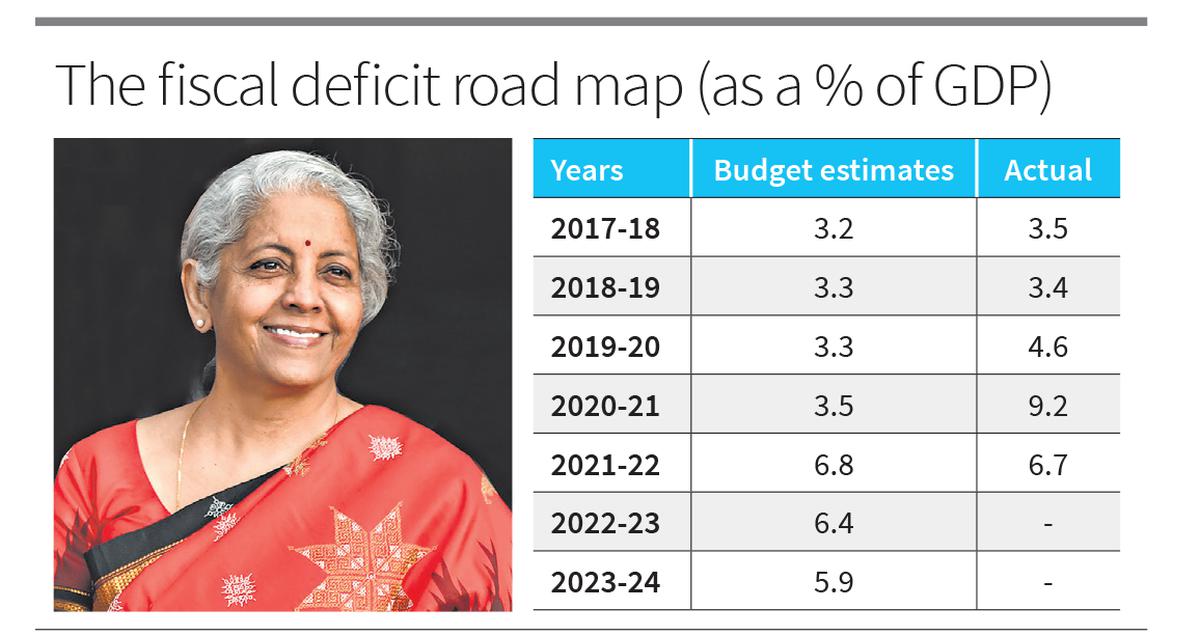

The story so far: In the Union Budget for 2023-24, Finance Minister Nirmala Sitharaman chose the path of relative fiscal prudence and projected a decline in fiscal deficit to 5.9% of gross domestic product (GDP) in FY24, compared with 6.4% in FY23. Ms. Sitharaman said the government planned to continue on the path of fiscal consolidation and reach a fiscal deficit below 4.5% by 2025-26. To finance the fiscal deficit in 2023-24, she said the net market borrowings from dated securities are estimated at ₹11.8 lakh crore, and that the balance financing is expected to come from small savings and other sources. The gross market borrowings are estimated at ₹15.4 lakh crore.

What is the direction on fiscal deficit given in the Budget?

In Union Budget 2023-24, the fiscal deficit to GDP is pegged at 5.9% in FY24. This ratio has declined from 6.4% in 2022-23 (revised estimate) and 6.7% in 2021-22 (actual).

In the revenue budget, the deficit was 4.1% of GDP in 2022-23 (revised estimate). In Union Budget 2023-24, revenue deficit is 2.9% of GDP. If interest payments are deducted from fiscal deficit, which is referred to as primary deficit, it stood at 3% of GDP in 2022-23 (RE).

The primary deficit, which reflects the current fiscal stance devoid of past interest payment liabilities, is pegged at 2.3% of GDP in Union Budget 2023-24.

Are allocations lower for some sectors?

The major allocations that have been pared down are food, fertilizer and petroleum subsidies. The food subsidy in 2022-23 (RE) was ₹2,87,194 crore. In 2023-24, it has been reduced to ₹1,97,350 crore. Similarly, the fertilizer subsidy in 2022-23 was ₹2,25,220 crore (RE); it has been reduced to ₹1,75,100 crore for FY24. The petroleum subsidy in 2022-23 was ₹9,171 crore (RE); it has declined to ₹2,257 crore in 2023-24 (Budget estimate/BE). However, the point to be noted is that compared with BE 2022-23, the decline is not that sharp. In BE 2022-23, food subsidy was ₹2,06,831 crore; fertilizer subsidy was ₹1,05,222 crore, which was less than what has been allocated in BE 2023-24. It is a laudable decision to extend food security to the poor for one more year amid rising inflation. However, rationalisation of subsidies is important so that the government can move towards reaching a fiscal deficit target of 4.5% by 2025-26.

What needs to be done for growth?

Inflation hurts the poor. The interest rate management by the RBI through inflation targeting alone cannot effectively control inflation, given the supply side shocks. Therefore, fiscal policy measures are crucial to tackle mounting inflation. Policy coordination between RBI and North Block is crucial for a sustained growth recovery process. The RBI has been increasing policy rates to tackle mounting inflation. But a high interest rate regime can hurt the economic growth process. So, the fiscal policy needs to remain “accommodative” with focus on gross capital formation in the economy with enhanced capital spending, especially infrastructure investment. In Budget 23-24, capital spending is expected to rise to 3.3% of GDP. The interest-free loan of ₹1.3 lakh crore for 50 years provided to States should help them spend and boost growth.

Also read | Fiscal deficit touches almost 60% of full-year target at end-December

Ms. Sitharaman stressed that infrastructure investment has a larger multiplier effect on economic growth and employment.

Can the govt. stick to fiscal consolidation?

The Government has not deviated from the path of fiscal consolidation. In Union Budget 2023, the medium-term fiscal consolidation framework stated that there is a need to reduce fiscal deficit-GDP ratio to 4.5% by 2025-26 from the current 6.4%. There are revenue uncertainties in post-pandemic times and also geopolitical risks, mounting inflation, supply chain disruptions and energy price volatility. At the same time, the Government has kept the fiscal policy “accommodative”, and has undertaken capital spending to support economic growth recovery. The predominant mode of financing fiscal deficit in India is through internal market borrowings. It is also to be financed through securities against small savings, provident funds and an insignificant component of external debt. In Union Budget 2023, India’s external debt is pegged at ₹22,118 crore of the total fiscal deficit of ₹17,86,816 crore in 2023-24 (BE), which is approximately about 1%. In Union Budget 2023, it is also stated that the States will have to maintain a fiscal deficit of 3.5% of GSDP of which 0.5% will be tied to power sector reforms.

What are rating agencies saying?

According to Moody’s, leveraging buoyant revenue, the Government plans to substantially increase spending on infrastructure, while cutting personal income taxes, and providing capital support for the oil sector. The Budget plans are credit positive for renewable energy companies, cement and steel producers, oil marketing companies and automakers in particular, it said.

While continued gradual fiscal consolidation contributes to the stabilisation of the government’s debt burden and supports credit quality, authorities remain unlikely to achieve their ambitious target to narrow the deficit to 4.5% of GDP by FY26, Moody’s added. According to Fitch Ratings, the slow fiscal consolidation process in the wake of the pandemic could leave public finances exposed in the event of further major economic shocks.

What lies ahead?

The Finance Minister is focusing on economic growth recovery through capex. She contends that infrastructure investment will boost private investment. In the fiscal deficit-GDP ratio, if the denominator GDP expands, it will reduce the overall fiscal deficit-GDP ratio. Her focus is on economic growth recovery to strengthen GDP.

Lekha Chakraborty is Professor NIPFP & Member, Board of Management, International Institute of Public Finance (IIPF), Munich